GameStop, a video game and consumer electronics retailer, is not a popular retailer in the stock market. Of 9 analysts covering the name only 1 has a buy recommendation. Incredibly, the short interest in the name (the amount of shares borrowed to sell short) equates to all the shares outstanding. It is very unique to see this consensus bearish positioning, creating a very power technical if there a fundamental change. We believe that management are delivering on such and the latest announcement of a deal with Microsoft (Xbox) and GameStop is a sign of further progress. This could get very very painful for the shorts.

Who are GameStop?

GameStop is an American video game, consumer electronics and gaming merchandise retailer. The company is headquartered in Texas and operated 5,509 retail stores throughout the United States, Canada, Australia, New Zealand, and Europe as of February 1, 2020. The company’s retail stores primarily operate under the GameStop, EB Games, ThinkGeek and Micromania-Zing brands.

The shares have doubled – what am I missing?

The street has been wrongfooted here. Earlier in the year this was seen as a higher default risk with the bonds trading at 70 cents in the dollar. A new management team had arrived in 2019, they are incentivised, the directors have purchased equity and the management team are delivering. The latest announcement with Microsoft means GameStop is now participating in the future revenue benefit of online games and digital merchandise after someone buys an Xbox in their store. People have asked is this a retailer or an e-commerce play (the answer is both..).

The Microsoft news last week caused the shares to rally 30% on a single day. Are there more announcements to come (with Sony and Nintendo) and despite rising significantly this year, could GameStop rally from $14 to $30 or even $40+? Let’s find out…

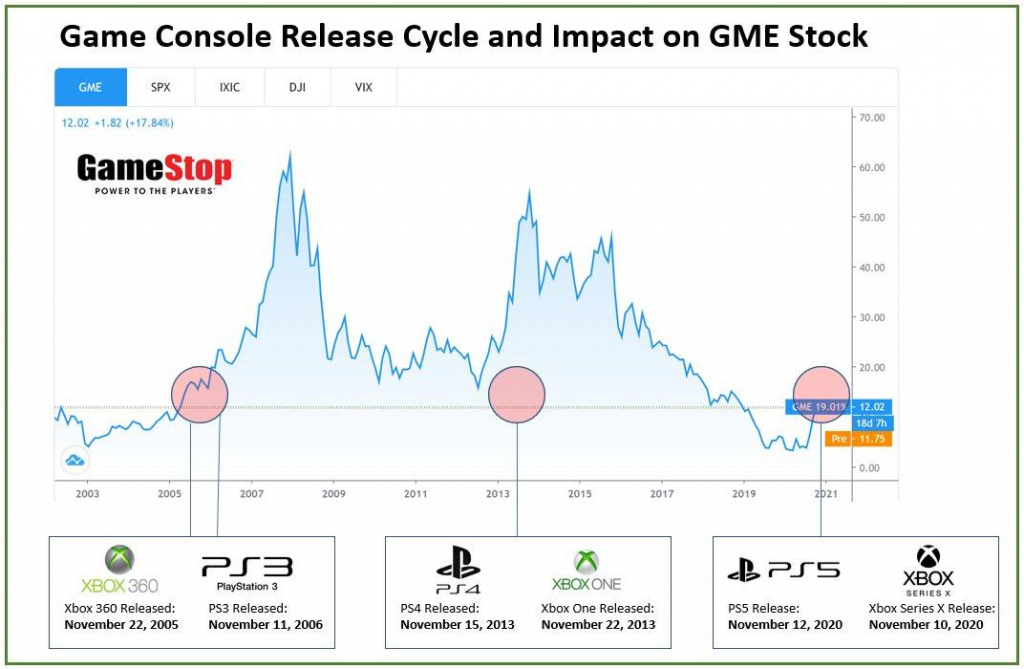

Get ready for the new 7 year console cycle with PlayStation and XBox ahead of Black Friday and Christmas.

This console cycle is significant and one can read about the full technical developments and the difference between PlayStation and Xbox here : https://www.techradar.com/news/ps5-vs-xbox-series-x . There is also speculation that there could be a new Nintendo Switch Pro in early January. In previous cycles this has been very supportive of the share price of GameStop. With launches coming in November and lockdown impacting at home entertainment, accelerated demand globally for consoles will be significant.

Image credit – Nave Young

It is important to note that console sales are no longer about standalone hardware units, where demand will exceed supply (waiting lists are building) but also software sales where games can be purchased physically, online and downloaded from the cloud.

What gets people excited about GameStop is that rather than just being a physical retailer it also becomes an ad-targeting platform to support vendors, publishers and merchandise makers. This omni-channel strategy will focus on creating a platform and a gamer community that focuses on physical and online games sold per console, expert gamers, eSports trends, ‘try before you buy’ and high attach rates (i.e if 300,000 of a new gaming title are sold into 1m consoles then the attach rate is 30%).

But isn’t all this going online and into the cloud? Why do you need a store? Its not all about online. Older games and collectibles (do you stream a vinyl?) are becoming a factor and you need a physical console to play such. Not all publishers will provide their games online/cloud based. The management argue that 260mn people across US, Canada, Europe and Australia are within 15 minutes of a store and people should be able to shop in terms of what is easy for them and they should be channel agnostic. When stores re-opened in the US this year, they said they didn’t see a shift from e-commerce back to store and the e-commerce trend held. More below.

The technical set up is explosive..

Despite the shares having doubled this year and being overbought short term – the technical set up is still very strong. The chart points to a share price breaking out of a multi-year downtrend and with rising volume. Another important point, is to watch gaps – these are breaks between opening and closing prices in the market where no trading takes place and leave a vacuum. Years of experience would show that a lot of the time gaps close and having reached $14, the next gap that has not closed would be $31, followed by $44…We will briefly explore if arriving at this share price level is justified fundamentally.

What has changed since 2019?

Firstly, since Summer 2019 there has been a complete refresh of the management team and Board at GameStop. In September 2019 they announced a comprehensive turnaround plan called GameStop ReBoot with 4 elements 1. Optimized the Core Business 2. Become the Social / Cultural Hub for Gaming 3. Build a Frictionless Digital Ecosystem and 4. Transform Vendor Partnerships.

This is a serious management team, they have reduced debt, repurchased share, sold non-core business units, cut SG&A, improved inventory and reduced working capital and started to wind down operations in the Nordics.

This has caused a serious change in investor appetite..this could add to the technical squeeze

In April 2020, Scion Capital Management (Michael Burry, for those that have watched the film the Big Short) disclosed he had increased his position considerably. He is now 4% of the company and GameStop is 17% of his last 13-F disclosures (30th June 2020).

In June 2020, given the actions by management and the balance sheet improvement Moody’s, the rating agency upgraded the debt. In August 2020, Ryan Cohen, founder of Chewy which was sold to PetSmart for $3.5bn in 2017 took a 9% stake in the company around $5 saying it was “significantly undervalued”.

Blackrock is 17% (of which a portion is ETF/indexed), Fidelity is 15%, RC Ventures is 10%, Scion is 4% and another hedge fund Senvest is 5.5%. This means that 40% of the register are large active holders that may not sell. Who is the marginal seller? Isn’t this what happened when high short interest met large holders in Tesla…the difference here is that GameStop is coming out of a distressed situation and the shares are undervalued versus other retailers, so quite different in that regards. But regardless, bears should learn from the technical. Furthermore, as the shares rally Vanguard, Dimensional Fund, Blackrock representing 25% of the share register have to buy more. And the latest short interest data is 68mn shares short versus 65mn shares in issue. Not to draw a fundamental comparison but this was a factor with Tesla shorts getting swept up in passive and retail flow with Musk, Ballie Gifford and Larry Ellison owning almost 30%. As the Tesla short interest went from 218mn shares in June 2019 to 55mn shares current the shares went from $37 to $498. This GameStop squeeze could get very painful.

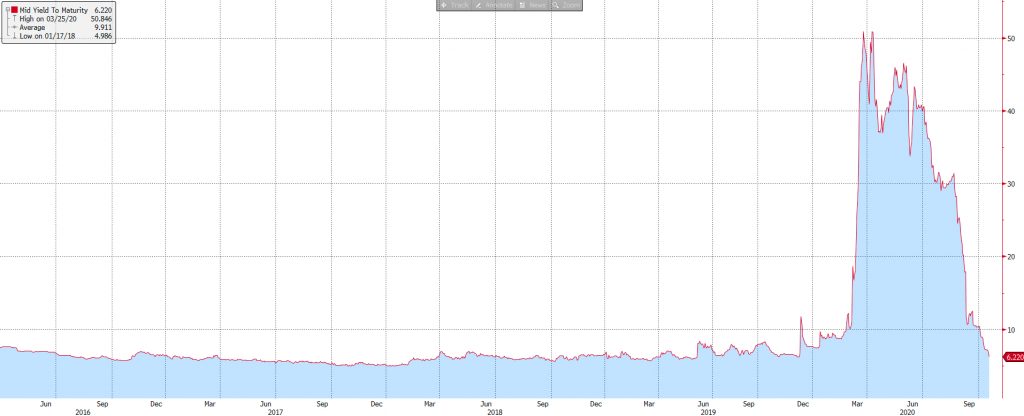

When the bond market changes its opinion, equity investors should pay attention…

The bond market had a significant change of view during the summer. Equity markets often misprice changes in a company’s cost of capital and credit spread. This is not the first time we have seen a distressed name normalise its corporate bonds and the equity market misses the inflection point. If you look at GameStop’s corporate bond issues spreads started to normalise significantly over the summer. Under real option theory, equity is a call option on the firm’s overall value and the change in the value of the equity can often be misinterpreted. Traditional sell side analysts still focused on earnings when the capital structure has been completely repriced. This happened a lot in 2008 to 2010, both positively and negatively with the banks and indebted equities.

How are the financials evolving?

Their Q2 2021 results (quarter end August 2020) where better than expected with same store sales down 13% despite the COVID19 meaning that there were 13% fewer store operating days and also the fact that it is the end of a 7 year console cycle and people will be waiting for new hardware and games. Their e-commerce growth has been a major deveopment and the shift to e-commerce will support their platform strategy and the digital ecosystem. Global e-commerce sales rose 800% for the quarter and went from low single digits to over 20% of total sales – they see this as a long term and post COVID trend. The CEO said that e-commerce should be a $1bn business and they said they will cross that trajectory in 2020. Omnichannel remains important and 90% of online purchases with pickup in store were fulfilled within 24 hours.

This will all mean that for year end January 2021 revenue will trough and looking out that GameStop is forecasted to see a revenue growth phase for the first time since its 2012 peak. Revenue is expected go from $5.7bn (FY Jan 2021) to $5.8bn (FY Jan 2022) to $6.2bn (FY Jan 2023) and generate EBITDA of $73mn in FY21, $160mn in FY 22 and $160mn FY 23.

The current market cap is $900mn and the company has $735mn of cash on the balance sheet and $1.1bn of debt as of the last quarterly update. The bond market as discussed is relaxed on the company’s credit position and the rating agencies have upgraded during the summer. They have managed working capital excellently so cash flow generation has been good recently. This may reduce with the console cycle and more money getting tied up in inventory again.

Is there a further disposal coming in Europe? There has been some speculation on this point. To January 2020, Europe represented 17% of Revenue ($1.1bn) and to date the main action has been closing Nordics. There is speculation they may sell the European business and now with the start of the console cycle it would make sense if they could sell the business at 0.3 or 0.4 of revenue to Jan 2022 it would bolster liquidity further from a region that even in 2015 and 2016 generated limited operating profits.

Trying to understand the Microsoft / XBox deal from last week.

The reason the shares are moving ahead of the brokers is the news from Microsoft last week is generating a lot of speculation on future profitability. In the last generation console cycle (2013 to 2019) GameStop generated $22bn of gaming product sales (video game software, hardware). Its hard to know if GameStop will replicate this deal with Nintendo or PlayStation.

How does it work? Lets say a new X Box X costs $499, the typical margin is around 10% so that is $50. However, what if a customer takes a monthly package such as the All Access package and doesn’t pay up front for the console and can access games from the cloud : https://www.xbox.com/en-US/xbox-all-access#findaretailer that is $35 per month. So that is estimated to be a 10% rev share with GameStop at $3.5 per month which will be $84 margin over 2 years instead of a one off of $49. When you start considering $25bn or $30bn of total sales over a console cycle that becomes really significant. 5 million XBox X passes could be $210mn of pure margin per year for 2 years. This compares with forecasted EBITDA in January 2020 of $167mn.

Does a subscription package cannibalize physical game sales? Not necessarily, game publishers will not all participate in the online model and physical games have a value for trade-in and you can also buy pre-owned games in store/online. Also, online gaming requires a broadband capacity that not all gamers have available when competing with other devices in the home.

The big question now is if Microsoft (Xbox) announcement is followed by Sony (Playstation) or Nintendo the revenue and earnings transaction could continue to shift.

So what’s it worth and could this squeeze continue?

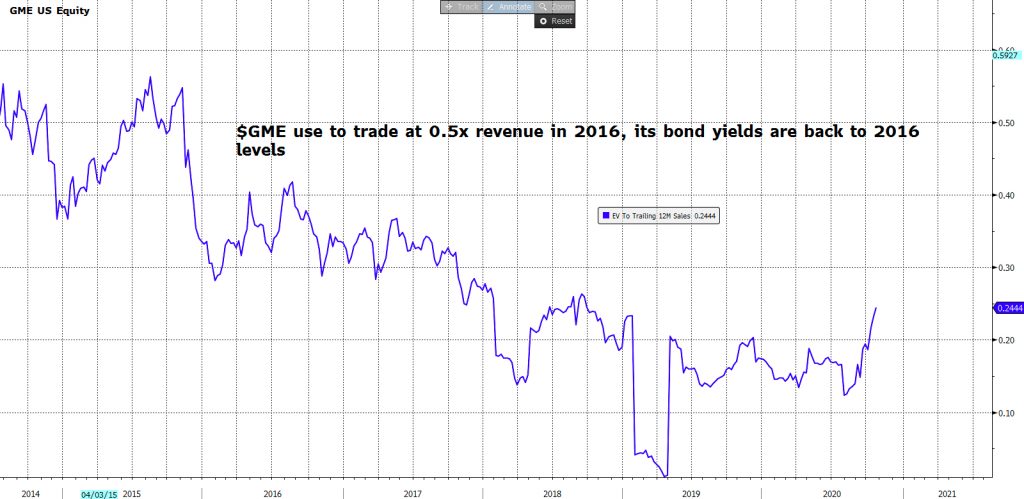

Let us start with a very basic analysis using EV / Next Year Revenue of 0.5x versus Best Buy at 0.65x. Best Buy is coming from a better place with 3% and revenue growth and EBITDA margins of 8% versus GameStop with revenue at a low and 6% EBITDA margin latest quarter. However, if the management can get GameStop revenue growth back on track, which is what the market is telling you, and keep improving EBITDA margin then 0.5x is very achievable and where it traded in 2016.

How how high can the shares trade? The market is clearly behind here, so we will take the highest analyst revenue estimate to January 2022 of $6.5bn. At 0.5x EV/revenue this points to an enterprise value of $3.25bn. This is a company that has done 8% EBITDA margin in the past so $500mn of EBITDA and 6.5x EV/EBITDA does not sound crazy (it traded at this multiple in 2015). Current Net Debt is $365mn, which would imply an equity value of $2.9bn. The shares outstanding are 65mn giving a fair value of $44 per share. Ironically, this is the technical gap in the chart from November 2015.

Conclusion?

Shorts be warned, there is no marginal seller of shares here and this could run hard towards $44 if GameStop gets back to historical EBITDA margins and multiples on more optimistic revenue assumptions. The console cycle starts in November, watch for more announcements and December 10th results.

Subscribe for stock updates as they are published – The Collective Finance

Read more – The potentially massive GameStop short squeeze outcome

Research

Lot’s more to follow….

The Collective are a panel of stock enthusiasts writing about high conviction investment opportunities with high return potential.

Visit our website for more.

12 thoughts on “GameStop ($GME): A squeeze to $44 from $14 can be justified fundamentally…100% of the shares are short. Watch out.”