Dividend yield and growth is very far from the average investor’s mind these days! Combine the exponential growth of Robinhood, Revolut, e-Toro copiers, CFDs, weekly options and binary options with lockdowns, mobile phones, social media and government cheques and short term retail speculation is the order of the day.

The Collective want to go the other way. This week we show a worked example of how we can take some parts of the market that may appear dull on first review and turn them into high returns in a tax efficient way.

We wrote in our opening piece on the inflation series that it is time to start considering dividend income and dividend growth with rising inflation risks. Why was this? Bonds and fixed coupon payments have served us well in a low inflation/deflationary environment and fixed income has been an excellent investment for decades. However, as previously written, we believe a regime change is coming and in a rising inflation environment you want inflation protected yield such as growing equity dividends.

Subscribe for stock updates as they are published – The Collective Finance

Bubbles are forming in parts of the market

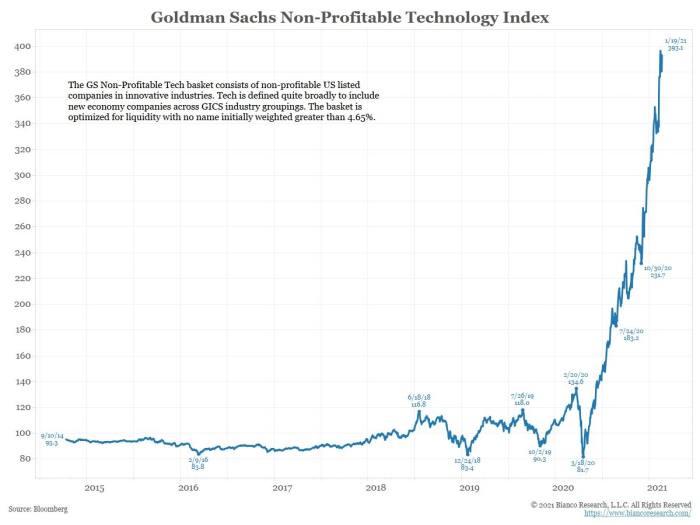

One does not have to look too hard in the financial press or on social media to find signs of excess. We are all reading about about SPAC’s, Bitcoin, short squeezes like $GME or $AMC, the parabolic rise of loss making concept stocks or “$1 shares”. We believe this is indicative of a clear bubble and is giving The Collective flashbacks to 1999. The chart really stood out to us, and was recently flagged at FT.com, to highlight the parabolic move in public loss making companies.

What we want to focus on is the part of the market that nobody is playing in like telecoms and energy sector where there are 6% and 7% dividend yields (with dividend growth). We see a large margin of safety here, these are not crowded or speculative positions that have been pushed far above intrinsic value by social media driven euphoria. If anything, we would be happy to use the next market drawdown and market volatility to add to these names at a higher dividend yield [Noting that at the time of writing the VIX is getting to a level where it has made sense to add exposure]

But these names are boring, I can’t post on social media that I made 100% in a day ! By turning a spread betting / CFD account on its head, we will show you how you can use conservative gearing and earn private equity like returns over a 2 year holding period (the investment time horizon of The Collective) with some of these dividend names.

We will illustrate this with an example of Orange, the French telecom stock, which has a 6.5% dividend yield. More fundamental detail on this name will follow in due course. Of course, this can apply to any the other high div yield/growth names we have been writing about (TP ICAP, Headlam etc)

Short term trading – the house always wins!

A quick reminder, especially in current times, when our judgement gets clouded by our neighbour telling us about the latest tech share or bitcoin trade they made money on via their mobile phone trading app.

Short termism is being compounded by short term observations and modern technology.

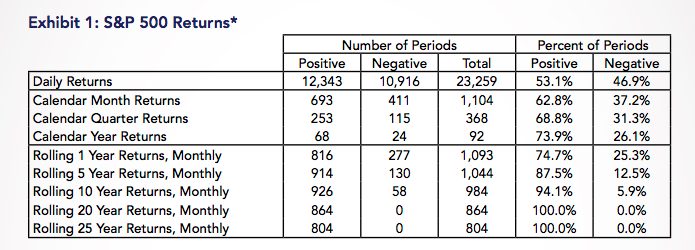

Why is this important? Very simply – if you observe the market less than daily your likelihood of a return is 50/50. If observed every 3 months that becomes 69% and once you get to 5 years it is 88%. On a 20 year holding period, we have not seen a negative period and that allows for some pretty significant speculative bubbles like 1929 and 1999 (and who knows where today will be ranked in market history)

Dividend yield names have really lagged and are seen as boring…when has cash flow ever been boring?

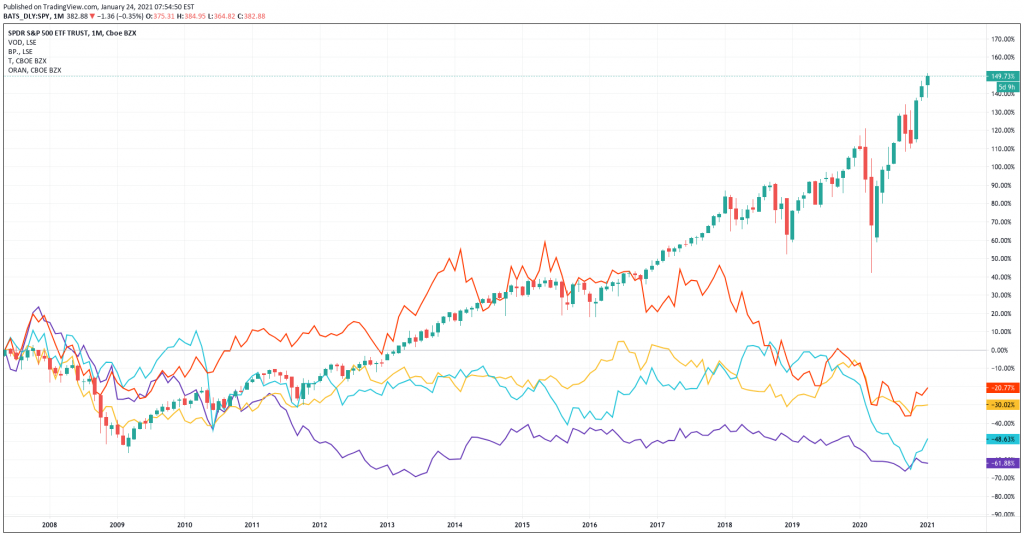

In a world where we need income that, importantly, will benefit if there is rising inflation there are an abundance of large cap names. Take a look at the extent of the lag of large cap names with 6% yields are more versus the S&P 500. We don’t think it takes much to cause a rotation here.

Is there a different way? Turn off your phone and think like a Private Equity partner.

We are going to show you with some pretty conservative gearing how you can generate a 2 year IRR of 25% + and a cash return on cash of 40% using a spread betting account but holding for 2 years and not day trading or speculating. This is buy and hold.

Here are our assumptions:

- Choose a stock with a dividend yield > 6% where the dividend is covered by earnings and cash flow and can grow by 5% per annum in line with earnings.

- Use 50% gearing i.e if the exposure is €20,000 the investment is €10,000 and €10,000 is borrowed. Very conservative versus what most people do.

- Being very conservative, the share price appreciation per annum from January 21 to January 23 is 7%. For context, that is 5% earnings growth and 2% inflation.

- The funding cost for the position is LIBOR + 2%. Note the funding is charged on the entire position. We don’t think Central Banks are going to raise rates on a 2 year view and will allow the economy to ‘run hot’.

- Dividends are credited to your account on the ex dividend date at the gross amount (not taxed).

- There may be tax benefits to this which our readers can check.

What return can I earn?

See our table below on what this means for a worked example like Orange. But this could apply to Exxon, BP, Vodafone, BATS, AT&T or other blue chip high yield names, this is just one example. What is key is to ensure that a high dividend yield is not implying a dividend cut or no growth. As a rule of thumb, once you get above 5% you need to do your homework as the market could be telling you something. Here are the numbers using actually confirmed funding rates with a provider.

| Orange SA (ORE.PA) | Jan-21 | Jan-22 | Jan-23 |

| Share Price | € 9.59 | € 10.26 | € 10.98 |

| Dividend Paid during the year | € 0.60 | € 0.63 | € 0.67 |

| Total Exposure | € 20,000 | € 21,400 | € 22,898 |

| Number of Shares | 2086 | 2086 | 2086 |

| Investment | € 10,000 | € 10,000 | € 10,000 |

| Amount Borrowed | € 10,000 | € 10,000 | € 10,000 |

| Funding Costs (LIBOR + 2%) | € 440 | € 471 | € 504 |

| Dividends Received Gross (ex date) | € 1,260 | € 1,323 | € 1,389 |

| Cash Flow (Investment + dividends – funding) | € (9,180) | € 852 | € 885 |

| Divestment Proceeds after borrowed amount | € 12,898.00 | ||

| IRR | 27% | ||

| Cash ROI | 46% |

Conclusion

These are very conservative numbers. We believe some of these names could rebound and deliver 15% to 20% share price appreciation per year. We are then getting towards 100% returns and close to the criteria for The Collective of doubling our invested capital on a 2 year view. Stay tuned for more ideas in the dividend yield and dividend growth area.

If you are enjoying the write ups and insights please sign up here for our emails: The Collective Finance

Collective Finance Research

Collective 2020 performance and market outlook

The Collective are a panel of stock enthusiasts writing about high conviction investment opportunities with high return potential.