Market nerves relating to COVID and the elections have driven risk levels higher. We are not focused on short term daily calls, but some helpful observations amidst the noise and volatility:

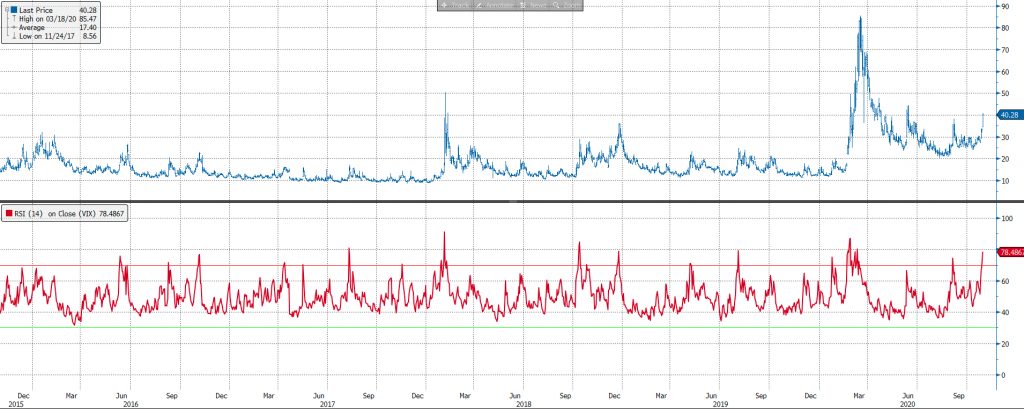

- The VIX index (a fear gauge) can be seen as a contrarian indicator. “Buy when others are fearful, sell when they are greedy”. Well, fear is high this week. Maybe an election result be required (or bring more uncertainty) – who knows. However, this is normally a level from where market volatility calms and has done so in recent years with central bank and liquidity measures.

- On the COVID front, ironically, we are days and weeks away from receiving news on a vaccines. Indications at this point are not “if” but more “when” , “who” and “how”. Markets normally look out 3 to 6 months and government authorities and pharmaceutical companies are playing the biggest game of expectation management in modern history.

- The latest is January for the US vaccine availability, which one has to expect will be the country that mobilises quickest on vaccine distribution. There was speculation this week that the AZN / University of Oxford vaccine increases immune response in higher risk groups in their phase 3 clinical trial. The expectation is their vaccine will be approved by year end. So lockdowns, to control the optics of cases in November, and then vaccine news in coming weeks does not seem fanciful.

- Will vaccines make a different to markets? It is difficult to see how people in high risk groups do not take these vaccines – they almost have a moral obligation to do such if they have been through the approved government processes. Get ready for the debate. However, indications are that 50% will and the impact and sentiment shift will be meaningful in our view.

- What of the stocks we have been discussing look interesting? None are particularly oversold yet. However, some quick observations:

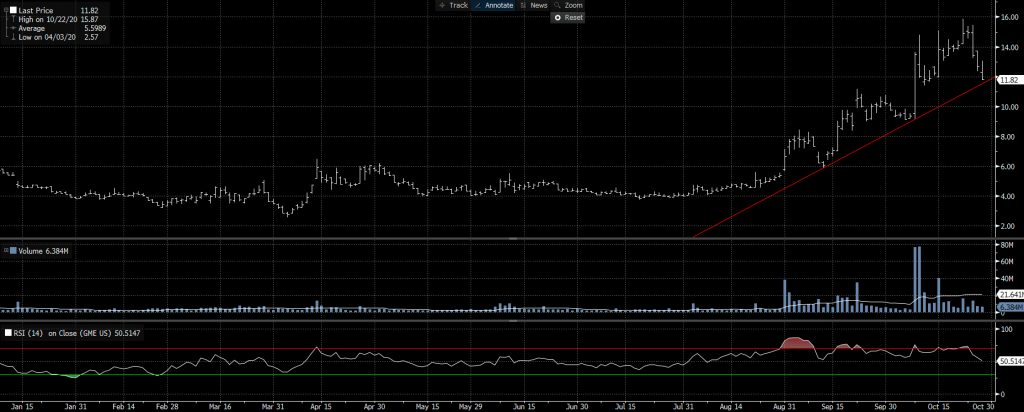

- $GME is now back to its trendline, and went from very overbought to almost oversold. There has been no fundamental change – if anything Microsoft and Sony this week have confirmed the early indicators of the strength of the console cycle. We will let the debate continue on omni-channel, store importance and digital versus physical games. Remain invested into a rising console cycle and December results.

- $HEAD.L – is not oversold yet. Note this month that the Chairman bought shares and last week over 2% of the company traded hands. Clearly a full lockdown is not good for their business in the UK, but the sector activity has rebounded.

- $MAB.L – Rallied 20% from our point of writing and became somewhat overbought. Everyone knows UK pubs are tough, the shares remain at multi decade troughs in price to book with a leading freehold estate.

- $HSW.L – Has rallied back with brokers out positive. See our previous note on why we think it should be an M&A candidate. The implied growth rate/rebound in the shares is non-existent looking out to next summer.

“We remain focused on our “post lockdown” series and companies that we see 100% upside looking out to 2022″

2 charts of note midweek. More to come.

Lot’s more to follow….

The Collective are a panel of stock enthusiasts writing about high conviction investment opportunities with high return potential.

Visit our website for more.