Mitchells & Butlers is trading at a 15 year low valuation. The current book multiple of 0.4x is not warranted for a company that covers it’s cost of capital through the cycle. The group has the leading freehold backed pub estate in the UK and we believe that a price to book multiple of 1x is warranted. Furthermore, we don’t believe it needs to raise capital with cash to hand, renegotiated covenants and credit facilities available. If Mitchells & Butlers trades at book it provides 100% upside as we revert to more normal trading level in pubs in 2021 and 2022.

Chart 1: At 0.4x price to book, we are an all time low value for Mitchells since 2004

End of lockdown – we will go back to the pub.

Please refer to our original note (Part 1 Hostelworld) for the rationale for this series. In summary, we believe we are in a “casedemic” that is far less dangerous and the pandemic is over in both the UK and Europe. As a result, lockdowns are not sustainable and will increasingly be questioned. In this series, we examine industry leaders that we believe will recover post lockdown. Last week we discussed the online travel agent for hostel bookings, Hostelworld. This week let us discuss the deep value case for Mitchells & Butlers, the leading freehold pub operator in the UK.

The 10pm curfew – a poorly conceived concept

After re-opening in July with reduced capacity, the UK pub sector has been hit again with a 10pm curfew in the UK from 24th September. The new 10pm closing hours for pubs has been met with a lot of resistance. People coming out of a venue at the same time has obvious implications. Instead we are seeing a ramp in house parties and people socialising in a way that is less regulated and riskier than the prior pub guidelines. The impact on pub trade has been significant with some areas seeing a 1/3 collapse in revenue in the week following the new curfew.

Are pubs and restaurants a culprit in the spread of COVID cases? It is very clear it depends on the circumstances – nightclubs and close contact for extensive periods is clearly contagious (Korea, Spain and Austria are all examples) versus distanced tables, table service being very different.

The industry is clearly frustrated given the measures it has taken and the evidence pointing to case spreading under controlled circumstances was limited. Furthermore, people’s compliance with lockdown restrictions is withering as many simply don’t see the underlying risks in their community. On the second day of the curfew Oxford Street in London turned into a street party – with masses congregating outside pubs. We struggle to see how this curfew is sustainable and is doing more harm than good at a health and economic level.

Mitchells & Butlers – an industry leader at trough valuation

Mitchells & Butlers (MAB.L) runs 1,800 pubs across the UK under the brands All Bar One, Harvester, Browns Restaurants, O’Neills amongst others. It is a sector that has seen serial acquisitions, takeovers and mergers since the 1950’s. By 1989 pubs (and their brewery owners) were seen as too concentrated and breweries were forced to divest their pubs under the 1989 Act. This caused a series of leverage private equity backed groups to emerge, that used leverage to create super groups such as Punch Taverns. Effectively, we went from concentrated brewery owners to concentrated public and private equity backed owners.

For the last 15 years, Mitchells has been seen as one of the higher quality operators along with Greene King (which was acquired by CK Asset Holdings, Lee Ka Shing, in 2019). Mitchells has typically covered its cost of capital and with 80%+ of the estate being freehold there is strong appeal with obvious avenues to optimise the estate as the freeholder.

Over the last 30 years the number of pubs in the UK has been a decline but in the last 2 years we have seen stabilisation both nationally and in London and even in some areas, like the North East, seeing an increase. The pub offer has evolved with more of a food offer and a gastro element to meet changing customer requirements – you can see this in the employment data by type with food servers versus pub staff growing. What will COVID mean? 2020 will surely see more declines in numbers/closures with weaker players with poor offerings, weaker financials exiting. There has been some movement of pubs to ‘alternative use’. The agent Fleurets has a wealth of information if you wish to get into the detail:

https://www.fleurets.com/market-intelligence/media/jan2020_surveyofpubprices.pdf

65% of pubs that go to auction remain as pubs, the remainder go to alternative use. This will benefit the operators that survive, like MAB, where their estate has been stable in the last 2 years with a strong offer and branding.

Recent trading and cash position

No surprise that is has been a roller coaster of a 6 month period for the company. Starting in September 2019, like for like sales were +0.9% in weeks 1 to 24 of the year (for food and drink), weeks 25 to 40 all venues were closed, weeks 41 to 44 (July) were down 32%, August was more stable at +1.4% with the UK government supporting (Eat Out to Help Out) but up to 19th September there was more weakness.

What does this mean? Can a pub cover its cash costs with curfew related trading? Yes, is the answer. It is brutal though, there are interviews with pub owners saying they are clearing £10 per day on reduced staff. It is a more straightforward operation for an independent owner or a freeholder but it does come at a severe cost to the food and drink suppliers and the staff. Young’s, an operator of 270 pubs in the south of England, said last week it will have to make 500 of its 4,200 staff redundant by the end of October. Fuller’s, another quoted play also will let 10% of its staff go. With 100,000 pubs, bars and restaurants in the UK it is a significant employer with 450,000 people estimated to be employed by the industry.

Will the company make any profit this year? For its H1 to April 2020 the group generated £97mn of operating profit – a severe decline versus £132mn in the prior year period. Analysts expect that the full year operating profit will fall to £40mn before rebounding to £200mn for the full year to September 2021. If the company can finish this annus horribilis with an operating profit it would be a great result.

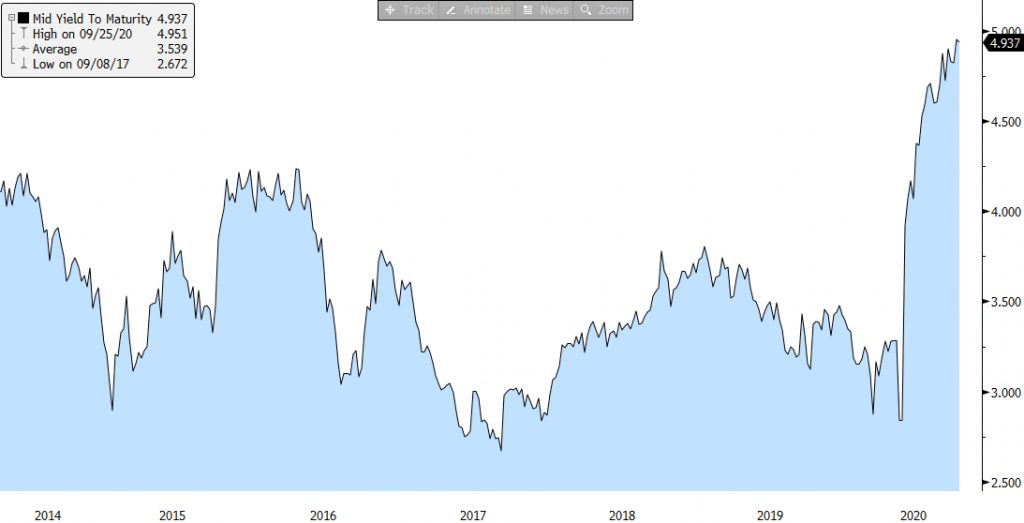

To date the bond market has remained subdued on the name. There is a 6% coupon 2028 bond issued in 2003 at £100 – it currently trades at £104 with a 5% yield, so no sign of deep concern from the bond market currently despite all the headlines and restrictions.

Chart 2: To date the corporate bond market are not stressed…2028 bonds trade above par with a 5% yield

The property backing of a freehold pub business

Given its estate is 83% freehold, the company has always been able to support a high level of debt. The Net Debt / EBITDA is normally 4 to 5x but will be elevated this year with the decline in EBITDA. The company has recently negotiated its covenants with the debt holders to allow for the abnormal COVID events.

In addition, there has been an updated property valuation done and provided with their half year results (6 months to April 2020). Property, Plant and Equipment was valued at £4bn in April 2020 comparing with total debt at that date of £2.8bn – this represents 70% Loan to Value which does not appear to be excessive. Pubs are valued at what is called Fair Maintainable Trade (FMT) and a multiple placed on such. For Full Year 2019 the company had around 400 pubs in the lower bracket of £200k per annum of FMT and around 160 of these were valued at 6 to 8x. This could mean the carrying value is hundreds of thousands of pounds up to to £1.5mn. While its estate has been stable in recent years, there is always the option as freeholder to dispose of underperforming pubs at a premium to carrying value.

Will Mitchells & Butlers need to raise money?

The cash position of the company at April 2020 was £190mn. Last week with its 24th Sept pre-close trading statement it discussed cash balances of £100mn and additional unutilised credit facilities of £140mn. Clearly it has been a very challenging 6 months and the company has suspended capex programs to conserve cash. The consensus is this year, after capital expenditure, it will burn £80mn of cash flow. It does look unlikely that any external capital will be required – but it should not be forgotten that it is has very significant shareholders (27% Joe Lewis, Piedmont, and 23% John Magnier and JP McManus, Elpida) if such a requirement arose.

Conclusion

Mitchell & Butlers is an industry leader with a well positioned freehold estate in the UK. The business has levers it can pull to support cash flow through these turbulent times. A prolonged period of trading disruption is more than priced in with a 15 year low in its price to book value. We believe Mitchells & Butlers can trade at book value again as trading recovers in 2021 and 2022, representing 100% upside. Time to start accumulating.

The Collective Finance research

The GameStop Short Squeeze is coming

Lot’s more to follow….

The Collective are a panel of stock enthusiasts writing about high conviction investment opportunities with high return potential.

Follow us on Twitter or visit our website for more.

11 thoughts on “5th October 2020: The “Post Lockdown Series”. Part 2: Mitchells & Butlers (MAB.L). You can’t download a pint. 100% upside.”