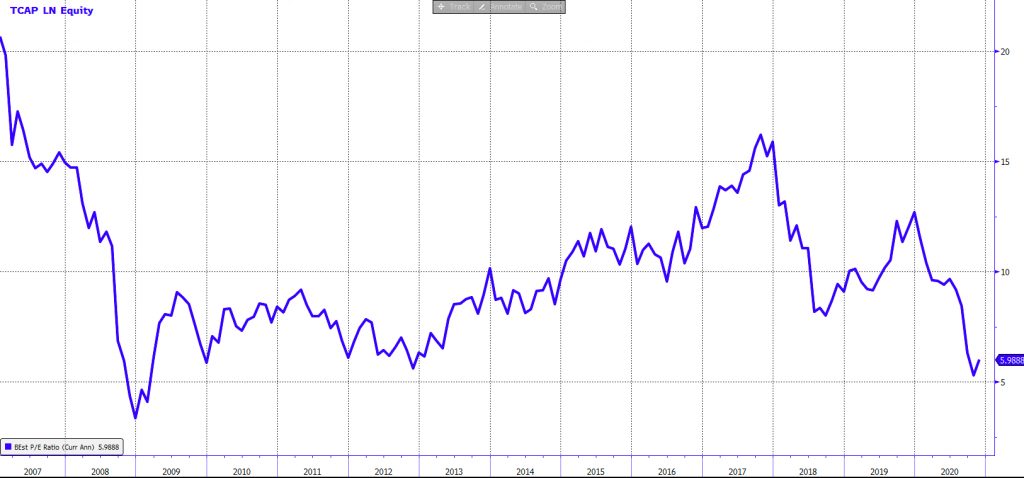

TP ICAP is a leading securities broker that is seeking to shift into higher growth and higher margin activities like electronic trading and data distribution via acquisition. The company has had a turbulent 3 years with Brexit, the Tullett Prebon integration of ICAP stuttering, rising costs and the ongoing shift away from voice broking. The valuation is close to an all time low and one has to go back to 2008 and the Great Financial Crisis to observe the shares trading at sub 6x forward earnings i.e the current valuation.

Currently, there is a technical factor suppressing the share price as a significant rights issue is imminent to raise money to purchase Liquidnet (a dark pool liquidity provider) – an acquisition that, subject to certain conditions, will complete in Q1 2021 and fill a number of key strategic gaps for TP ICAP.

We believe that once the transaction concludes in Q1 2021 the shares will re-rate in subsequent quarters out to 2023. Data centric listed exchange companies (Nasdaq, CME, Euronext) trade at 20x earnings or more and pure electronic trading peers (TradeWeb and MarketAxess) trade at 40 to 60x earnings. The Liquidnet transaction will assist on both fronts in terms of an improved electronic trading and data offering.

If TP ICAP can deliver on post deal strategic objectives the shares should trade at 12x earnings as a higher margin and higher growth business. This would mean the upside potential is significant looking out to 2023. In addition, you are ‘paid to wait’ with a 2021 and 2022 dividend yield of 4% and 8% respectively, while the company executes on the integration of Liquidnet. This would point to a fair value of 550 pence versus 214 pence currently.

Liquidnet acquisition announced in October 2020

Liquidnet has its origins as a leading ‘dark pool’ operator. Dark pools allow large blocks of shares to trade ‘off stock exchange’ and reduce share price impact. In recent years Liquidnet has increased its presence in fixed income, trade analytics (OTAS acquisition), data analytics (Prattle acquisition) and fund manager offerings (Research Exchange acquisition).

In October 2020, when TP ICAP announced its intention to buy Liquidnet for a potential total consideration of up to $700mn, the market was initially unimpressed given the acquisition was 10x EBITDA, a premium to TP ICAP, and funded by a large rights issue with no earnings accretion for a few years.

However, we believe the market is missing what this could mean for the future of TP ICAP from a technology, electronic trading and data perspective. Companies that are skewed to these revenue verticals do not trade at 10x earnings (the historical multiple for TP ICAP) but trade at 20x, 30x or more.

There is a very strong synergy from the Liquidnet acquisition and it will enhance TP ICAP presence on the buyside (i.e with funds) rather than just inter bank trading, increase its presence in equity and off exchange liquidity, enhance its exposure to electronic trading and accelerate its ability in data and analytics. The full strategic rationale for the deal can be viewed here:

The rights issue and deal conditions

The deal timeline has been well articulated in an October 2020 release. The transaction is subject to:

- Shareholder approval: circular and prospectus to be published in January 2021

- Completion of re-domiciliation: introduction of a new Jersey-incorporated holding company

- Transaction expected to close in Q1 2021 pending customary regulatory approvals

Will there be anti-trust issues? There is limited overlap between the businesses with Liquidnet focusing on buy side (fund managers) and equities execution via ‘dark pools’. This is at odds with TP ICAP’s strength in interbank and fixed income, derivatives, rates and commodity related broking.

The October release states that the company needs to raise $425mn / £320mn of equity via a rights issue. This is significant versus its current market cap of £1.2bn. If this was done at £1.90 subscription price (a 12% discount) the number of new shares would be considerable, at 168 million new shares, versus a current share count of 566 million. This coupled with the temporary reduction in the dividend explains a lot of the share price weakness.

Insiders have bought in recent weeks…

As you know from The Collective framework, we like to see insider buying and put significant weight on a management team or board member putting money to work, even when the amounts are small. We would note that we have seen 4 smaller insider transactions (open market purchases) in the last 7 weeks.

What does a combined TP ICAP and Liquidnet look like?

The company provided some detail in early October on the deal rationale and future profit margins. This allowed some sell side brokers to have a first attempt at what a pro-forma business could look like. Brokers are penciling in £500mn of EBIT and £350mn of profit after tax in FY 2023. This is based on the combined Liquidnet and TP Icap revenue lines and getting to a post completion EBIT margin of 20%.

A £350mn profit after tax and increased share count of 734mn shares would point to an earnings per share of 47 pence in 2023. Something that Tullett Prebon has not achieved since 2006 / 2007 when it first listed on the London exchange.

What is the dividend yield?

In 2018 and 2019 the company paid £94mn and £95mn of dividends respectively. In order to reduce the dilution of the rights issue the company has said that it will reduce the 2020 dividend by 50% to £47mn. It then expects the dividend policy going forward to be a 50% payout ratio (2x covered by earnings). So on the reduced dividend for 2020 it is on a 4% div yield, then 8% on the recovered dividend. However, if 47 pence eps is achieved then a 23 pence dividend in 2023 would point to a future yield of 10%+. In summary, the share price will be supported as it goes through this transition. [Note: fixed income markets are confident with TP ICAP 2023 bonds trading at a yield of 2.4%]

What is the right earnings multiple?

This is where it gets interesting. TP ICAP between 2019 and 2022 is expected, pre Liquidnet, to be around a 3% revenue growth and 16% EBIT margin business. The company is guiding a 20% EBIT margin post Liquidnet integration. The revenue segments being emphasised in the new business are not 3% growth.

- Fixed Income electronic trading – this has lagged equity market electronic trading in terms of adoption and is double digit growth or more based on MarketAxess and Tradweb.

- Data & Analytics – this is an existing revenue segment for TP ICAP but will be enhanced by Liquidnet and should be 10% revenue growth.

The significant hidden asset is the amount of data that TP ICAP has to distribute and sell. Data revenue as a % of total revenue in TP ICAP lags its exchange trading focused cousins. For TP ICAP, data is a 50% margin business versus group margins at 16% currently. In 2019, TP ICAP data revenue is 9% of total, CME is 11%, Euronext is 19% and Nasdaq is 31%. Where will TP ICAP data revenues be in 2023?

The company wants at least 50% of its future revenue to be in higher growth segments and coupled with a higher profit margin we do not believe a 15x earnings multiple is excessive. The early pro-formas are pointing to 15% earnings growth which would be a P/E ratio to eps growth (PEG) of 1x. All very reasonable. However, we will be conservative and use 12x.

Conclusion – the shares could get back to their 2018 highs of 550p versus 215p currently.

If the company achieves its 20% EBIT margin by 2023 the earnings per share could be 47 pence. At 12x earnings the shares would trade at their 2018 high of 550p

We believe that in the coming months the rights issue detailing and deal conditions being achieved will present a compelling opportunity to accumulate an increasingly data and technology driven business with significant upside. Furthermore, you are ‘paid to wait’ with a 8% dividend yield in 2022 (4% in 2021) as the management integrates Liquidnet over subsequent quarters. The asymmetry is very compelling.

Collective Finance Research

The GameStop Short Squeeze is coming

Lot’s more to follow….

The Collective are a panel of stock enthusiasts writing about high conviction investment opportunities with high return potential.